Morocco has the 6th largest economy in Africa. It also ranks 48th (out of 80) in the list of most innovative countries worldwide, according to Bloomberg (2016). Agriculture, tourism, aerospace, automotive, phosphates, textiles, apparel, and subcomponents, are the key sectors of the economy.

In the 1980s, Morocco was a heavily indebted country. However, under the reforms overseen by the IMF (International Monetary Fund) and since the Kingdom of Mohammed VI (1999) took place, Morocco managed to achieve a steady growth. Having significantly increased investment in transport and industry infrastructure, as well as having introduced free trade zones, Morocco improved its competitiveness in the last decades and managed to establish itself as a centre for doing business throughout Africa.

In 2015, Services contributed to the 57% of the Moroccan GDP, while Industry accounted for 29% and Agriculture for the remaining 14%.

Nowadays, it is worth noting that tourism is the second largest contributor to the national GDP, as well as employment (with 505,000 direct employees) in the country. In 2014, 10.3 million tourists visited Morocco, representing an increase of 2.4%, compared to 2013.

Mainly dependent on rain-fed agriculture, due to poor harvest in 2014, Morocco registered the lowest annual expansion, since 2000. In contrast, in 2015, the country’s economy registered a strong economic performance, with a 4.4% growth rate. It is predicted though that in 2016, this growth will decrease sharply (to 2.7%), but will thereafter stabilise to about 4% for the next two years (2017-2018).

Overall, mainly due to developments in the agriculture sector, Morocco’s growth has slowed down in recent years (from 4.6% in the period 2003-2012, to 3.8% over the period 2013-2015). It is worth noting though, that in the period 2012-2015, the country’s fiscal deficit decreased from 7.2% to 4.3% of GDP, and the account deficit from 10% to 2.3% of GDP.

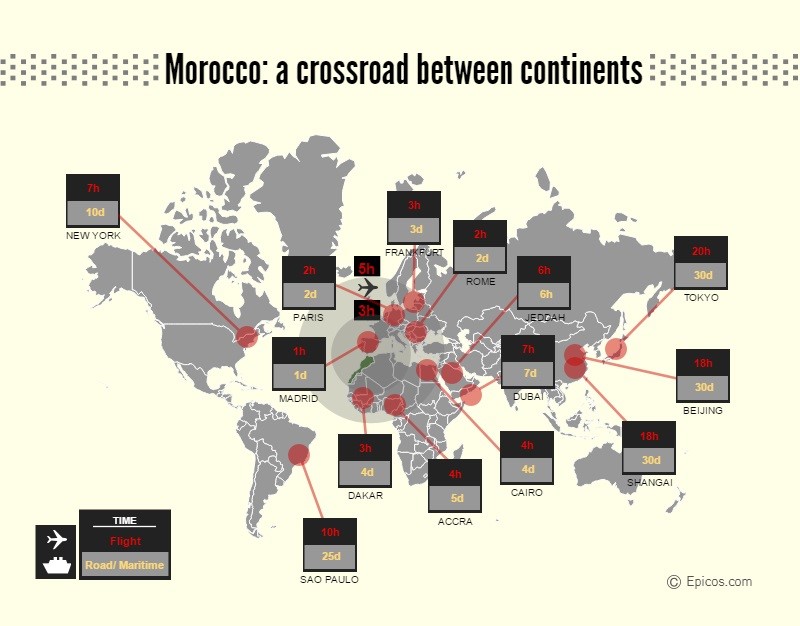

Taking advantage of its privileged geographic position –at the crossroads of America, Europe and the Arab world- Morocco has developed an extensive trade network, by air, sea and land, allowing the country to import and export goods, in a really short time.

In recent years, due to its strategic location on the globe, as well as some commitments and reforms that have taken place, Morocco managed to increase significantly its total trade transactions.

In real terms, after a significant drop of exports in 2009 -affected mainly by the economic crisis in the EU- exports have increased steadily, to reach DH215.3 billion (€19.7 billion) in 2015. In the same period, imports also increased, reaching a high of DH389 billion (€35.5 billion) in 2014, before dropping to DH367.3 billion (€33.5 billion), a year later.

In 2015, as a result of the aforementioned, the trade deficit decreased to DH152 billion (€13.8 billion). In fact, the decline of imports in 2015, was coupled with significant reductions in energy (-DH 26.5 billion) and food products (-DH 6.1 billion) imports, while the respective increase in exports was related to increases in automotive sector (+DH 8.4 billion) and phosphate and derivatives (+DH 6 billion) exports.

Morocco has one of the most open services trade regimes in the world. However, the absence of a services sector regulation, leads to low rankings when compared to other regions of the world. As per the provisional balance of payments for year 2015, the Moroccan Services sector exhibited a trade surplus of about DH62 billion (€5.7 billion). Related revenues included Travel services (DH44 billion), Telecommunication, computer and information services (DH12.1 billion) and Manufacturing services on physical inputs (DH 12.1 billion).

In fact, due to the bilateral agreements with the EU (DCFTAs) and the Euro-Mediterranean Partnership (Euromed), Morocco managed to become a worthy trade partner of the EU market, with 46% of Moroccan exports destined to Spain, France and Italy, in 2014.

Moreover, it should not be omitted to mention that on the other side of the Atlantic Ocean, under the Free Trade Agreement (FTA) signed in 2006 between Morocco and the US, trade between the two countries has increased up to date, by some 300%.

In the same year (2014), the worldwide exports of Morocco, were mostly related to clothing and textiles, automobiles, electric components, chemicals, transistors, crude minerals, fertilizers (including phosphates), fishery, fruits and vegetables.

In terms of imports, the main suppliers to Morocco of foreign commodities, in 2014, were Spain, France, China and the US.

These imports mainly included crude petroleum, textiles, telecommunication equipment, gas and electricity, transistors and plastics.

The Deep and Comprehensive Free Trade Agreement (DCFTA) between the EU and Morocco, signed on the 1st of March of 2013 – concerning the trade in services, government procurement, competition, intellectual property rights and investment protection- has helped Morocco to reinforce its presence in the EU market (See chart below). Today (2015), the EU is the main trading partner of Morocco, with the total amount of transactions in goods (imports and exports) reaching €30.7 billion.

More specifically, the main exports to the EU, included machinery and transport equipment, manufactured articles (mostly textiles/clothing) and agricultural products, while Moroccan imports from the EU consisted mostly of machinery and transport equipment, manufactured goods, chemicals and related products, and fuels and lubricants.

Source: http://trade.ec.europa.eu

In terms of trade in services, Morocco had a trade surplus of 1.6 billion in 2014, as a result of the significantly increased related exports (by €600 million). These changes reflect the increased turnover of the tourism sector, as well as the development of the offshoring sector.

Despite the improved poverty rates as aforementioned, and also according to the International Monetary Fund, which has found that poverty has decreased considerably (by 40%) in the last decade, high unemployment, poor living conditions, and lack of economic opportunity, are still present in Morocco. More specifically, despite the growth over the past three decades, labour force participation rates still remain low, compared to other emerging markets. In 2013, the unemployment level had dropped significantly compared to that of twenty years ago (from 13% to 9%). However, as a result of the slowing economies in the EU – Morocco’s main economic partner- and the country’s unpreparedness to absorb an increased number of workers entering the market, overall unemployment increased to 10.2% (with the youth unemployment above 15%), in 2014. Having already registered a drop in the related figure since 2015, predictions forecast that the unemployment rate will further decrease to about 9.3%, by 2020.

Morocco has been the recipient of more than US $500 billion of inflows of Foreign Direct Investment (FDI), between 2010 and 2015, which have been used for infrastructure development, structural reforms and macroeconomic policies. Under these developments, it is worth noting that a number of multinational companies –including the sectors of automotive, electronics, aerospace, in recent years have moved their regional headquarters to Morocco.

According to World Bank’s “Doing Business 2016” data, Morocco ranks today 75th worldwide, as far as the ‘ease’ of doing business in the country, a major improvement when compared to the 115th position, five years earlier (in 2011). This remarkable improvement, is reflected in the increase of FDI inflows, as well as reduction of the average number of days needed to start a business in the country, which has dropped to 10.

Additionally, according to International Monetary Fund (IMF), Morocco’s banking system is working towards achieving the minimum requirement for the Liquidity Coverage Ratio (LCR) of 100% by 2019, compared to that of 60% in 2015. This requirement, ascertains, in broad terms, the financial position of the Moroccan companies’ and their ability to fulfil the obligations to their lenders.

Further, at the beginning of 2016, the IMF reaffirmed Morocco’s continued qualification to access PLL (Precautionary and Liquidity Line) resources. This has contributed to the consolidation of the market confidence in Morocco’s policy plans.

Morocco has implemented a series of strategies targeted at raising performance and revenue in key-earning sectors, while boosting employment, and attracting further foreign investment. Regarding the latter, the government has set a series of macro-economic policies and priorities regarding trade liberalization, as well as structural reforms and infrastructure development. In addition, taking into consideration that rising tax revenues as a proportion of national income, is key to African countries economic development, the Moroccan Government increased the total tax revenue to 28.5% of the GDP (in 2014). Moreover, through the Industrial Development Strategic 7-year Plan set by the government in 2014, government aims to strengthen the linkages between small businesses and the industrial leaders of the country, and also raise manufacturing GDP to 23%, while creating 500,000 new jobs in manufacturing, by 2020. Towards the aforementioned, Morocco has signed numerous bilateral agreements for the promotion and projection of investments, as well as the elimination of double taxation of income. Finally, on a different approach, to enhance the local economy, Morocco requires investors to use domestic goods and technologies when possible, and also through tenders in certain sectors, promote domestic interests, based on specific requirements.

On the other hand, despite the government’s steadily increased public spending on education, by 5% per year since 2002, reaching 5.9% of GDP, in 2014, existing skill-mismatches do not aid Moroccan competitiveness. While aiming to lead the agriculture, alternative energies and banking services sectors in the sub-Saharan region, as well as the fact that the local Automotive, Electronics and Aeronautics Industries are growing rapidly, Morocco’s labour demands for a highly educated workforce, will further increase. In order to further expand and reach to a certain point the fast growth of the MENA (Middle East & North Africa) region (as illustrated in the %GDP chart), it is essential to confront discrepancies between the academic and market-industrial needs, through further reforms in education.