The last ten years (2006-2016), economic growth in Egypt has been volatile. After the wide-ranging reforms that started taking place in 2004, private investment, as also foreign direct investment, increased, contributing to strong economic growth of the country. This acceleration of the economy was halted by the global financial crisis (2008-2009), when exports in goods and services slowed down, dragging down the overall growth, while also leading to an increase in the unemployment rate. After Al-Sisi took over governance (June 2014) and political transition occurred with the election of Representatives at the end of 2015, the Egyptian economy showed signs of recovery. Cash, loans and new business took place, while investment in infrastructure and measures targeting a more macroeconomic stability, came into effect. It is indicative that by the end of 2015, about 224,000 new jobs were created, while the inflation rate is expected to decrease from 10.1% in 2014, to 9.5% in 2017.

In 2015, as indicated below, about 46% of the total GDP was attributed to the Services sector, while 40% came from Industry, and only 14% originated from Agricultural activities.

It should not be omitted that Tourism contributes significantly to the Egyptian GDP. Being one of the world’s first nations historically, Egypt has a long heritage. Having contributed significantly towards developments in writing, agriculture, urbanization, central governance and religion, Egypt’s cultural legacy attracts a great amount of visitors every year (as shown in the table below); the astonishing-iconic monuments, such as the Great Sphinx, the Giza Pyramid complex –one of the seven wonders of the world- are open to visitors, as well as for archaeological study.

The Arab Spring (that was experienced in Egypt as of January 2011, as discussed in previous) and the expansion of terrorism during the political transition from 2013 onwards, have contributed towards the decrease of annual visitors to Egypt (especially from EU).

Despite the positive economic development that had been achieved until 2008 –reflected in the 7.2% GDP growth for that year-, the world economic recession impacted the growth rate trend, which was reduced to 4.7% of the GDP only a year later (2009), reaching the minimum of 1.8% of the GDP growth, in 2011.

During the following years (2012-2014), the percentage of GDP growth, stabilised to about 2%, increasing up to 4.2% in 2015, or in other words a GDP value of some current US $330.8 billion. Finally, it is expected that Egypt’s GDP growth, will follow an upward trend from 2017 onwards.

Egypt has recorded trade deficits for more than a decade, as imports have grown much faster than exports. In the last financial year for which data was available (FY 14/15), imports were increased to US $61.3 billion, while imports were calculated to only US $22.2 billion, increasing the deficit to US $39,060.4 million.

According to the Central Bank of Egypt and the General Authority for Investment and Free zones (GAFI), the main exporting commodities of Egypt include Crude oil & petroleum products, Finished goods (such as fertilizers, ready-made clothes, cotton textiles, articles of iron & steel and pharmaceutical products), as well as organic & inorganic chemicals and raw materials (e.g. potatoes, citrus fruits, dairy products, eggs and honey).

The main destinations for Egyptian exports in 2014-2015, were the EU (33.6%), followed by Arab countries (24.8%), Asia (14%) and the USA (9.8%).

On the other side, the main commodities that Egypt imports, include Machinery and equipment, auto parts, foodstuffs, chemicals, metal products, plastics and fuels.

The main trading partners for FY 2014/2015, in terms of imports to Egypt, included the EU (30.8%), Arab countries (19.1%), Asia (20.4%) and Russia (7.5%).

Despite the growth recorded in recent years, employment opportunities have been limited in this North African country. More specifically, according to data derived by the Ministry of Industry & Trade, a “paradox” (when compared with developed economies) seems to take place in Egypt; even though overall unemployment exhibits a decline –as happens overall in the Arab States-, in recent years, youth unemployment has increased significantly, despite the highly educated youth graduating from higher educational institutes.

Moreover, inequalities between sexes remain high, with almost 65% of women aged 15-24 being unemployed, compared to 33% of men.

Unemployment predictions reflect an overall drop of the unemployment rate, below 10%, by 2018. However, if current trends in the labour market continue, rising unemployment among younger Egyptians and low quality jobs on offer, will undermine productivity and overall economic development of the country. Therefore, associated reforms should focus on the development of governance, further private sector jobs creation, the elimination of social imbalances and the improvement of macroeconomic indicators.

From the 1990s till 2003, FDI inflows to Egypt had considerably decreased by 62%. However, after the adoption of significant reforms by the government, FDI grew till 2008, as a result of many related initiatives. Towards the aforementioned, the Public Private Partnerships (PPP) mechanism, was created in an attempt to boost the budget aimed for infrastructure development, effective also on private technology transfers. The establishment of the Egyptian PPP Law, was recognised as the best new law in the World, in 2010, and received great political support.

However, FDI flows followed later a drop of 72%, in 2013 – due to worldwide financial crisis and the effects of the Revolution in 2011.

The determinative role of the government during the last few years, has helped towards the restoration of confidence on investors’ part, and therefore has lead towards the increase of FDI inflows to Egypt.

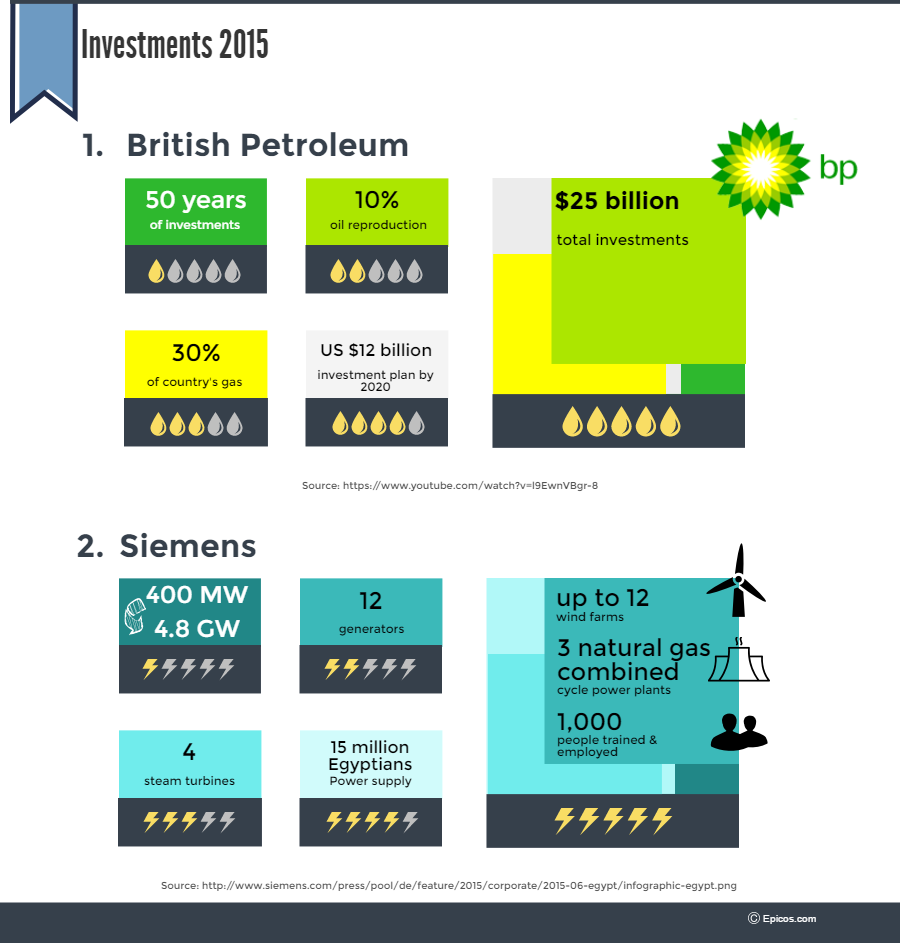

As a result, many international corporations have established subsidiaries in Egypt (See some related examples in the Infographic below).

In fact, under the presidency of Abdel-Fatah Al-Sisi, investments have returned to the country, helping the rebound of the GDP growth.

Indicatively, in 2015, a $12 billion contract was awarded to the British Petroleum (BP), for the development of gas fields in the West Nile Delta, by 2020. Through the implementation of this project, a significant 30% of the country’s gas production will be offered. In addition, in the same year, a deal of US $8 billion was signed with Siemens for the establishment of gas and wind power plants, in Beni-Suef, Burullus, New Capital, Al Miniya and Ras Ghareb. These investments will not only cover 15 million people’s power demand, but also boost the economic development of the region, by offering up to 1,000 permanent jobs and associated training (See Infographic below).

To further increase the exports and attract international investments, Egypt has been promoting the development of new specialised Free zones, apart from the ten (private and public) already established in its territory. Through these, technology transfer to the local industry and the generation of employment opportunities are expected to occur.

Finally, at the moment (2016), various large-scale projects are taking place, from infrastructure development, to the creation of innovative technology industries, the integration of civil and commercial centres throughout the Egyptian territory, the development of tourism and the introduction of new medical cities.

Unfortunately, despite the progress that has been achieved under the Al-Sisi’s presidency, the still ‘unfriendly’ regulatory environment for businesses -it is indicative that according to the World Bank’s “Doing Business” report for 2016, Egypt ranks at the 131st position (out of 189 economies)-, the extended bureaucracy and the elites connected with the political corruption, are still appearing as shadows that follow the economic growth of the country. In an attempt to eliminate the effects of the above, under the government’s economy (development) programme, a new Investment law has been approved in 2015. Moreover, in 2016, the Higher Council for Investment has been established and new incentives have been prescribed towards the further increase of investments.

Therefore, a new set of Macroeconomic goals have been set by the Ministry of Finance. These indicate that:

- Real GDP growth should pass 6% by the end of FY 2018/2019.

- A faster job creation rate needs to be achieved, to bring the unemployment below 10%. Focus will be placed on addressing youth unemployment.

- The fiscal deficit should be reduced to 8- 8.5% of the GDP, while the government debt to 80 - 85% of the GDP.

- Improvements in domestic investments and export performance should be achieved, as also as far as the development of human resources, through higher budgets allocated to Health, Education and R&D (over 10% of the GDP), by 2019.

- Upgrading of local infrastructure is considered essential.

Finally, the aforementioned should be implemented in combination with the development of governance, the creation of private sector jobs, and the elimination of social imbalances.