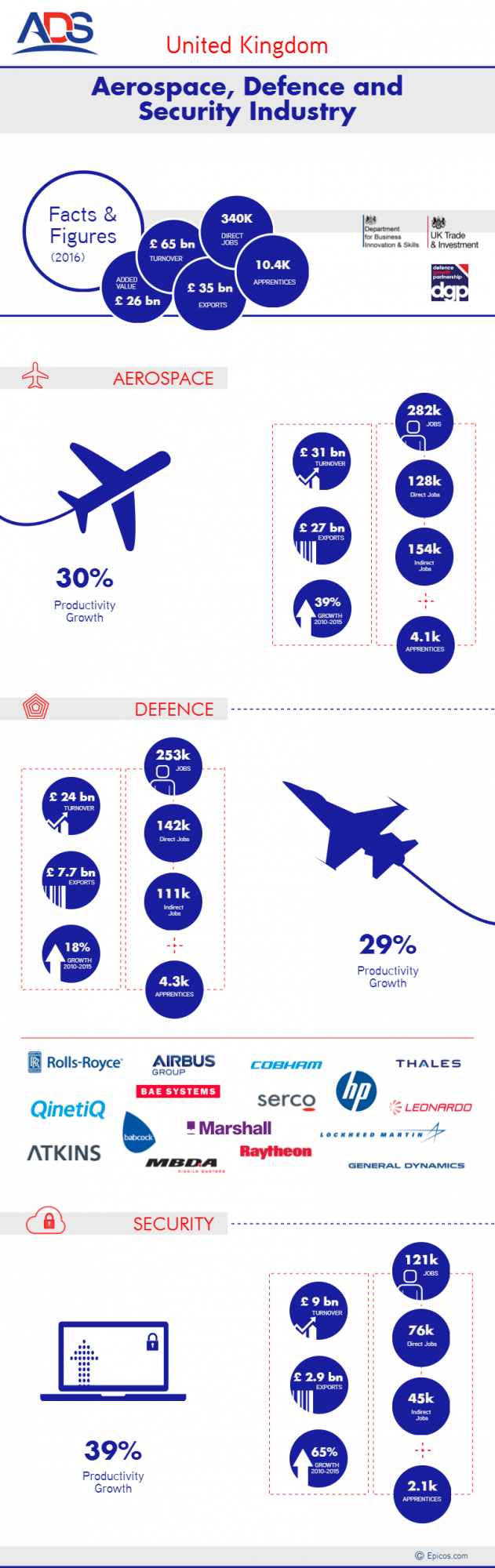

The UK’s Aerospace, Defence & Security industries deliver world-leading capabilities, vital to protecting national security and generating economic prosperity. In fact, according to the latest UK ADS (UK Aerospace, Defence, Security and Space trade organisation) Report, a total turnover of £65 billion, of which £35 billion were from export orders, has been achieved by the relevant industries, in 2015.

More specifically, as per the 2016 ADS report, the UK’s Aerospace Industry is the largest in Europe and the second largest worldwide (after that of the US). With 128,000 direct employees –25,000 are employed in R&D, Design & Engineering roles-, a 39% growth since 2010 (6.5% annual growth in 2015) and £27 billion exports (in 2015) –predominantly driven by sales to the US and the Middle East-, the UK Aerospace Industry had a total turnover of £31.1 billion (2015). The sector’s paramount contribution to the UK’s economy, is strongly reflected in the high growth rate of associated productivity, i.e. 30% over the period 2010-2015, when compared with the 2% of the rest of the UK Economy.

The UK’s Defence sector recorded (in 2015) a turnover of £24 billion –increased by 2 billion when compared to the 2014 revenue-, sustaining 142,000 direct jobs, 30,000 in research, design and engineering roles. With an 18% average growth (over the period 2010-2015) and a 29% productivity growth (over the same period), the sector recorded some £7.7 billion exports on average, over the period 2010-2014. Moreover, it should not be overlooked that nowadays the UK’s defence value chain is supported by over 5,000 SMEs, directly supplying the MoD.

Further to the aforementioned, the UK’s Security sector supports the UK’s economy with 76,000 direct jobs, £2.9 billion average exports (over the period 2010-2014) and some £9 billion in turnover (2015). In addition, the sector has enjoyed a 65% growth, since 2010.

Source: https://www.adsgroup.org.uk

Source: https://www.adsgroup.org.uk

Reacting to the projected global demand increase over the next few years, local A&D investments in Apprenticeships for Production roles have increased. On the other side, the importance of the Aerospace, Defence and Security sectors for the sovereignty and economy of Great Britain, continues to be highly recognised by the UK government. It is indicative that UK government has recently committed £1.3 billion funding for the Successor Submarine programme. This, will not only port technological advances that will ensure the deterrence of potential threats, but it will also lead to enhancements in the UK’s operating and infrastructure capacities, as well as new employment opportunities.

To reinforce the Industry’s initiatives, government efforts should further aim on attracting additional investments to the UK, improve productivity throughout the supply chain, ensure innovation and the implementation of the 2015 SDSR (Government’s Strategic Defence and Security Review) objectives, through additional funding for R&D, as well as removal of export barriers and identification of new market opportunities.

Moreover, foreign companies continue to demonstrate their confidence in the British A&D industry. It is indicative that Boeing doubled its UK workforce since 2011, and through investments aims at further increases. Characteristically, in October of 2016, 37 companies from Boeing’s UK supply chain, as well as Boeing itself –building on orders for the P-8A Poseidon maritime patrol aircraft and the AH-64E Apache- have committed towards the continuity of their collaboration and the further improvement of competitiveness of UK companies, while supporting more than 12,700 jobs in the tier-one UK supply chain.

According to the SIPRI database (2014), the top 10 UK arms-producers and military services-providers, included: BAE Systems (US $25.7 billion arm-sales), Rolls-Royce (US $5.4 billion) and Babcock International Group (US $3.5 billion).

|

UK Top arms-producing & military services companies |

Total sales, 2014 (in US $ Bn.) |

Arm sales %, 2014 |

Total Employment, 2014 |

|

BAE Systems |

27.4 |

94 |

83,400 |

|

Rolls-Royce |

24.0 |

23 |

54,100 |

|

Babcock International Group |

7.4 |

48 |

10,840 |

|

Serco |

6.5 |

33 |

118,620 |

|

Cobham |

3.0 |

61 |

12,710 |

|

QinetiQ |

1.3 |

91 |

6,250 |

|

GKN |

12.3 |

8 |

51,400 |

|

Thales UK |

1.9 |

50 |

6,420 |

|

Meggitt |

2.5 |

35 |

10,820 |

Source: http://books.sipri.org

In terms of Supply chain & Investment, it is worth noticing that the UK still remains at the centre of global defence supply chain investment. The percentage of defence companies with a UK-based supply chain increased by over 10% in 2015, while UK remained the largest exporter of defence equipment and services in Europe, and the 2nd –after the US- largest exporter worldwide, followed by Russia and France.

Considering that the growth of the UK Defence Industry is driven by exports, focus on entering in new markets (e.g. Middle East and Latin America), as well as continuation of exports to Europe, North America and China, is crucial for Great Britain’s Defence Industry, calling the British government to develop a more ‘active’ strategy to support export opportunities.

Within the context of a fast changing geopolitical environment and the increasing global trade competition, the UK Defence Industry needs to react quickly and adapt its military capability by producing more flexible systems and services, to preserve its competitive advantage. Towards this direction, exploitation of emerging technologies, as well as an ‘open-systems’ approach seem imperative. On a different approach, overseas customers often seek tailored solutions supported by the UK Government, for the provision of technology transfer, inward investment and local partnering.

Indeed, to take advantage of the innovation that may occur within Small Medium Enterprises (SMEs), the UK’s Ministry of Defence lately announced a new series of measures to reduce bureaucracy and enable better collaboration between them and the government; this policy should lead to a minimum 25% of both direct and indirect procurement to be spent with SMEs by 2020, compared to the 19.2% in 2015. Further to this, in order to encourage UK entrepreneurship and considering that the private sector cannot adequately support related research, the MoD recently (2016) set up a £800 million fund (for the next 10 years) for the development of disruptive new technologies –the MoD already spends £300 million annually for this purpose. The MoD’s focus is on increasing its unmanned vehicle capability, as well as promoting laser weapons’ development.